Early cost estimation for die casting

Proceedings of ICED 1995, Praha, Edition Heurista 1995, pp. 1007-1016

Torben Lenau and Thomas Egebøl

Abstract:

Cost is one of the most important evaluation factors when making decisions in design. But most methods available

today require detailed knowledge of the production method from the designer. This paper presents two algorithms for

cost estimation for the die casting process. The algorithms are tailored to be used in the early design stages and are

based on case studies in die casting companies as well as studies of process selection in design. The one algorithm is

very simple and assumes that the cost is proportional with the cost of the material. The other algorithm is more

comprehensive and covers die cost, material cost, cost of casting as well as additional processing.

Inhaltsangabe:

Kosten sind ein wichtiger Bewertungsfaktor für das Treffen von Konstruktionsentscheidungen in der Produktgestaltung.

Die meisten der heute verfügbaren und angewandten Methoden verlangen vom Konstrukteur ein detailliertes Wissen

über Fertigungsverfahren. Diese Arbeit bietet zwei neue Algorithmen zur vereinfachten Kostenabschätzung an. Diese

Algorithmen sind auf die Anwendung in frühen Konstruktionphasen ausgelegt und bauen sowohl auf Fallstudien aus der

Druckgußindustrie als auch auf Studien über den Auswahlprozeß des Fertigungsverfahren in der Konstruktion auf. Der

eine Algorithmus ist unkompliziert und setzt die Annahme voraus, daß sich die Kosten proportional zu den

Materialkosten verhalten. Der andere Algorithmus ist umfassender und schließt neben den Kosten für Form und

Formherstellung, Material und Gießprozeß auch die Kosten für die Nachbearbeitung und Weiterverarbeitung ein.

BACKGROUND

Many of the decisions influencing an efficient production of the products are taken in the early design stages. It is

therefore vital that designers and other people involved in these early considerations have access to the right information

about the production. Cost information is important for making the right decisions. A problem is though that there only

exist little cost information and calculation formulas which is suitable for early design work. This was shown in a

previous literature study where 41 papers about cost estimation were reviewed [1].

An algorithm which is used by designers as a help for decision making trough out the product development must be

made in such a way that the designers requirements are fulfilled. The designers normally expect such algorithms to be

easy and quick in use. Many of the existing cost algorithms require detailed knowledge about the production equipment

- knowledge which the designers normally do not posses. Furthermore are such algorithms often hidden in computer

programs which makes them less convincing to the designers. This is especially true if unlikely results occurs. In the

present work emphasis have therefore been put into avoiding production specific questions and into describing the

single steps in the calculation.

In most cases designers cannot be expected to have profound knowledge about die casting. The first algorithm is

constructed in such way that estimating can be done without any knowledge of the process. The other require a

minimum of knowledge of the process but does on the other hand give the user the opportunity to understand which

factors that influence the price.

To estimate the cost of die casted components many factors have to be considered. This makes the estimation process

very demanding and complicated. We have chosen to pick out the most important estimation criteria. These criteria can

be determined in the early stage of product development for which these algorithms are created to be used in.

The first algorithm is extremely simple. It is based on the hypothesis that the component cost and the material cost are

proportional. This give remarkable precise results. However it is not possible for the user to achieve an understanding

of which factors that affects the cost. The second algorithm therefore require that a number of cost factors are

specified. This includes consideration of machine hour rate, material costs, casting costs and deburring and costs for

other tools.

COST EVALUATION THEORY

Cost evaluation can be seen from different theoretical viewpoints. Especially the estimation of hour rates can be

debated. The theoretical problem lies in which cost elements should be included, e.g. direct labour and overhead. We

have chosen the pragmatic approach to use the market given hour rate, which can be determined by comparing

quotations from competing companies. It is our experience that there is a sort of general agreement about these rates.

METHOD FOR DEVELOPING THE ALGORITHMS

The algorithms are created on the basis of examinations of quotations and interviews in four Danish companies. The

second algorithm includes the same cost elements as used for calculating quotations but is changed so designers can use

it. Special attention have been put into estimating the cost of the die. The die cost is calculated considering the cost of

die material as well as the die complexity. We have chosen to keep the algorithm as close to common practice as

possible since this ensures the best estimates, as well as the designers understanding of which factors that influence the

cost.

Knowledge about the costing methods used within the companies were acquired by interviewing people from the

companies. By following them step by step in how they calculated quotations and by reviewing previous quotations the

rules behind the methods were identified.

Based on our own experience as well as previous empirical studies [2] of process selection in design the costing

methods were tailored to fit the designers needs.

THE FIRST COSTING METHOD

The first costing method can be called the volume based estimation method. It is very simple and assumes that the

component cost is proportional with the material cost as described by the formula

C = 2,36 * cost of the material + 5,13 (1)

This formula can calculate cost for aluminum parts on cold chamber casting machines. We assume however that the

formula can be applied to other materials and types of pressure die casting equipment as well. The cost includes

additional machining and profit and is equal to the price calculated in quotations. The formula is only suitable for a

production volume larger than 30.000. For smaller production volumes the tooling cost will have more significant

influence which the algorithm does not take into account.

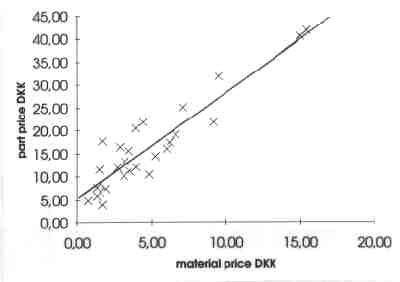

Figure 1. Evaluation of the first costing method

When results from the formula are compared with the cost for 28 components collected from four companies the

correlation factor is 0,92. In average the results were within 25 % of the collected prices and the maximum deviation

were 126 %. This means that the volume based method is suited for rough estimates of pressure die casted

components produced in medium to large volumes.

THE SECOND COSTING METHOD

The second costing method is based on cost calculation experience in die casting companies. Methods and examples of

calculated costs were collected from four Danish die casting companies. The second costing method estimated the total

cost of a component, i.e. it is equal to the price given in a quotation. The method involves 3 stages: Estimation of die

cost, casting cost and cost of additional tools.

Stage one - Estimation the die cost

The die cost is estimated by determining the die complexity, correcting the cost for the component size and finally by

determining the optimum number of die cavities.

Figure 2. Four categories of die complexity used for estimating cost of the die. Cost for each category is shown in table

1.

| Description of category | Die cost | Cost of extra cavities |

| Uncomplicated parts without cores. | 135 | 25 |

| Parts with some complexity, often without cores or with a few cores | 200 | 40 |

| Complex parts, often with one or several cores that move in the same direction as the die | 280 | 60 |

| Very complex parts, with cores in several directions | 350 | 80 or more |

Table 1. Die cost (cost in 1000 Danish kroner)

It is difficult to estimate a die cost without profound knowledge of die making which cannot be expected from a typical

designer. However, in the early stage of design the demand of accuracy is often limited to a rough estimate. We have

chosen to estimate the die cost on the basis of categories of complexity. In this way the designer does not need to have

knowledge about die making and the accuracy of the die cost estimate will be within 50.000 DKK from the estimate.

Figure 2 presents the four categories of complexity and table 1 shows the die cost.

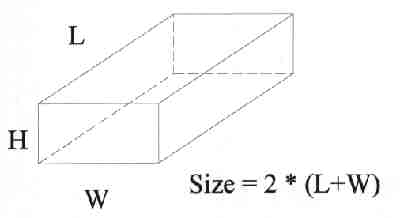

As the parts get larger more material has to be removed when the die is produced. The die cost

is influenced by this fact and can be corrected in the following way. The cost described in table 1 assumes the size of

the part is 670 mm. The size is calculated as the sum of the two largest dimensions for a circumscribed box multiplied

by two. For larger parts 0.6% should be added to the cost (including the cost of extra cavities) for each 1% the size

grows. For smaller parts 0.3% should be subtracted from the cost each time the die size declines 1 percent.

Figure 3. Part size is found as the sum of the two largest dimensions for a circumscribed box multiplied by two.

A die holds the same number of cavities as the number of components it can produce in one casting. It is very important

for the economy to use the right number of cavities. Every time the number of cavities is doubled, the machine cost is

reduced with nearly 50%. On the other hand the extra cavities cost extra. With the following expression the optimal

number of cavities can be found: (2)

(2)

(2)

The right hand side of the equation calculates the reduction in production cost when using more cavities than one. C is

the cost for the cavities and N the total number of parts to be produced. tc is the cycle time. a is the number of cavities.

S is the machine hour rate. r is the rate of interest in percentage per year and m is the number of months the die will be

used for production.

Stage 2 - Estimation of the casting cost

Before estimating the casting cost the machine hour rate and the material cost must be determined.

In the Danish pressure die casting companies it is common practice to calculate the casting prise as you calculate cost.

There is just one difference: The profit is included in the machine hour rates. The following rates applies to a 500 tons

cold camber machine with automatic feeding, manual lubrication and part removal, which is typical for Danish industry.

For each production batch the preparation cost for the casting machine is approx. 1000 DKK and additionally 200

DKK for setting up deburring equipment. When the machine is producing, the machine hour rate is approx. 370 DKK.

The hour rate for deburring by cutting and vibration, grinding and sorting is approx. 190 DKK. If the degree of

automatization is higher the machine cycle time will normally decrease and the machine rate will increase nearly

proportional. Therefore it will not affect the prise of the casted part.

The weight of the component is estimated using the component volume. The density of aluminium is 2750 kg/m3 which

is sufficiently precise since the normal alloys for casting have almost the same density. To the material price 8% should

be added for waste. Furthermore about 1 DKK per kg. is added to the material price (which at the moment is 14,50

DKK per kg) to cover the delivery costs, overheads, storage cost for the die casting company.

Material cost = Part weight (kg) x 1,08 x 15,50 (dkk/kg) (3)

The casting cost per part can be expressed by the operating costs of machinery per part and is therefore proportionally

to the operation time of machinery per part. Establishing the cost for casting is therefore the same as establishing the

operation time of machinery. At the same time we assume that the operation time of the machine will not be influenced

by the number of cavities. If there is more than one cavity in the die, the operation time has to be divided with the

number of cavities to get operation time per part.

Figure 4. Three categories of component complexity used for estimating casting price.

We have found that cycle times can be handled by using cycle times for three categories of component complexity as

described in figure 4. Category 1 consists of simple parts with little thickness. Category 2 consists of parts with some

complexity. Sometimes they contain cores which move in the same direction as the die. Category 3 consists of parts

with great thickness and/or complexity sometimes with several cores that do not move as the same direction as the die.

The time used to complete the cycle in seconds for the categories are showed in table 2. The times given are for a cold

chamber machine. For a hot chamber machine the times are approx. 50% lower.

| Machine specification | cat. 1 | cat. 2 | cat. 3 |

| manual | 60 | 70 | 90 |

| + automatic feeding | 50 | 60 | 75 |

| + automatic lubrication | 35 | 45 | 65 |

| + automatic part removal | 30 | 40 | 55 |

Table 2. Cycle times in seconds

The casting price can then be calculates using (4)

![]() (4)

(4)

The runners and the gate leads the floating material into the cavity where the part is formed. These runners and gates

have to be separated from the part. If runners and gates are large (more than 5mm), they have to be cut of using cutting

equipment. When runners and gates are of normal size but special caution has to be made, separation can be made by

hand. Processing times depend on if special caution have to be paid. Processing capacity for the separation can be seen

in table 3.

| Size of runners and gates | |

| Large (>5mm) (large parts or parts with thich sections) | 100 |

| Normal size, special caution (visible breakage point) | 200 |

| Normal size, no special caution | 200-500 |

Table 3. Capacity for separation of runners and gates (parts per hour)

Deburring by cutting removes burs on the die separation line. This is normally done with all parts and processing time is

about 250 parts per hour. Deburring by vibration is a grinding process which removes sharp edges etc. Almost all die

cast parts are deburred in this way. We recommend the following guiding figures of productivity:

1. Small parts in sizes up to 5 cm: 700 parts per hour

2. Normal parts in sizes up to 10 cm: 450 parts per hour

3. Parts of a larger size: 250 parts per hour

Sometimes further deburring or grinding is required but general guidelines are difficult to point out. The cost increases as

the dies get worn out because of flaws caused by heat appear. For the most the conditions are first made clear when

the production is settled. We have descided to add 2 DKK per part to cover these extra cost elements. We

recommend this figure to be used unless special aspects are obvious.

Stage 3 - Pricing of additional productions tools

Stage 3 concerns the price of other production tool. In connection with deburring of the parts several fixtures and tools

can be required. The cost for this step vary and we recommend that this is budgeted for 25,000 DKK.

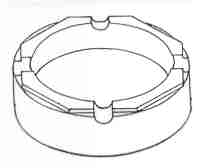

Example: Price estimation of an ashtray.

As an example in using the method the price for the ashtray in figure 8 is calculated. This ashtray is not a typical die

casting part because of its great thickness. 50.000 ashtrays are to be produced during 2 years in 25 batches. The rate

of interest is fixed at 12% per annum. The weight of the part is to be 320 gram.

| Die cost, form category 1, table 1 | 135 |

| Cost for cavities: 4 cavities•25.000 | 100 |

| Size correction: 60 % smaller than 670 mm, 18% is subtracted from the cost | -42,3 |

| Total die cost: | 192,7 |

Figure 4. Ashtray. Table 4. Ashtray example, stage 1,

die cost in 1000 DKK

The number of cavities is determined in (5) by using formula (2). (5) calculates the cost reduction by using 2 cavities

instead of one. The cycle time is found in table 2 as 90 seconds (the ashtray is very thick). The machine hour rate is

370 DKK.

![]() (5)

(5)

The cost of using four cavities is 4•25.000• 0.82 DKK = 82.000 DKK which is less than 182,000•(2/4). Five cavities

cost 5•25.000• 0.82 DKK = 102.000 which is more than 182,000 (2/5). Four cavities are therefore chosen.

In table 6 the total cost is calculated to 16.65 DKK per part. In comparison we have calculated the cost using the first

algorithm in (6). For the ashtray the two algorithms give similar results.

C = 2,36 * 320/1000 * 15,50 + 5,13 = 16,84 (6)

| Material cost 0,320 (kg) * 1,08 * 15,50 (dkk/kg) | 5,36 |

| Casting cost 1/4 * 90 (s) * 1/3600 (s/h) * 370(dkk/h) | 2,31 |

| Sorting and separation 190 /200 parts | 0,95 |

| Deburring by cutting 190 / 250 parts | 0,76 |

| Deburring by vibration 190 / 450 parts | 0,42 |

| Grinding and deburring | 2,00 |

| Casting cost | 11,80 |

Table 5. Ashtray example, stage 2, casting cost in DKK

| Batch cost per part 1200 * 5 / 50.000 | 0,60 |

| Die cost per part, stage 1 192.700/50.000 | 3,85 |

| Other production tools, stage 3: 10.000/50.000 | 0,20 |

| Casting cost, stage 2 | 11,80 |

| Total Cost | 16,65 |

Table 6. Ashtray example, part calculation scheme, cost in DKK

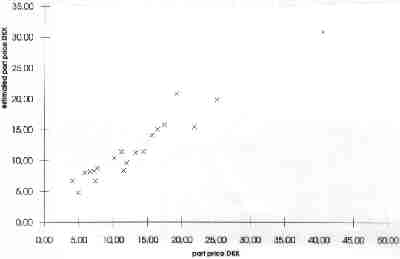

EVALUATION OF THE METHODS

The two methods can be evaluated with respect to two criteria namely the quality of the methods and their value for the

designer. Cost figures from the first method were compared with quotation prices from the companies in figure 1 and

the results were quite good. The method is very simple and the estimated cost was within 25 %. However the method

can only be used for medium to large production volumes. Furthermore does the method not supply the designer with

information of which factors that influences the cost.

The second method is evaluated in figure 5. Quotation prices collected from the companies are compared with

calculated costs. In average are the calculated cost within 18% of the collected prices and the maximum deviation is 67

%. The correlation factor is 0,96. This method require that the designer answers more questions, but does on the other

hand give insight into which factors that influences the cost. Many of these factors are production specific, but emphasis

have been put into showing how they can be translated from the knowledge that designer have about the product in the

early design stages.

CONCLUSION

Two cost methods for estimating the part cost using the pressure die casting process are presented. Both methods are

useful for the designer in the early design stages since they provide rough estimates sufficiently precise for the

preliminary comparison of manufacturing opportunities.

Figure 5. Comparison of collected prices and cost calculated by the second method.

References

1. T. Lenau, Jan Haudrum: Cost evaluation of alternative production methods, Materials & Design Journal, vol 15.

no.4. August 1994, pp. 235-247.

2. J. Haudrum: Creating the Basis for Process Selection in the Design Stage, PhD-rapport, Procesteknisk Institut, The

Technical University of Denmark, August 1994.

Acknowledgement

This work was made possible by support from the Danish Technical Research Consil under the program for integrated

production systems (IPS).

Address:

Torben Lenau and Thomas Egebøl

Institute of Manufacturing Engineering

The Technical University of Denmark, Building 425

DK-2800 Lyngby Denmark

Phone +45 4525 4811 Fax +45 4593 3435

![]()

This page was last updated on 29.05.1996, Torben Lenau, Thomas Nissen, DTU.